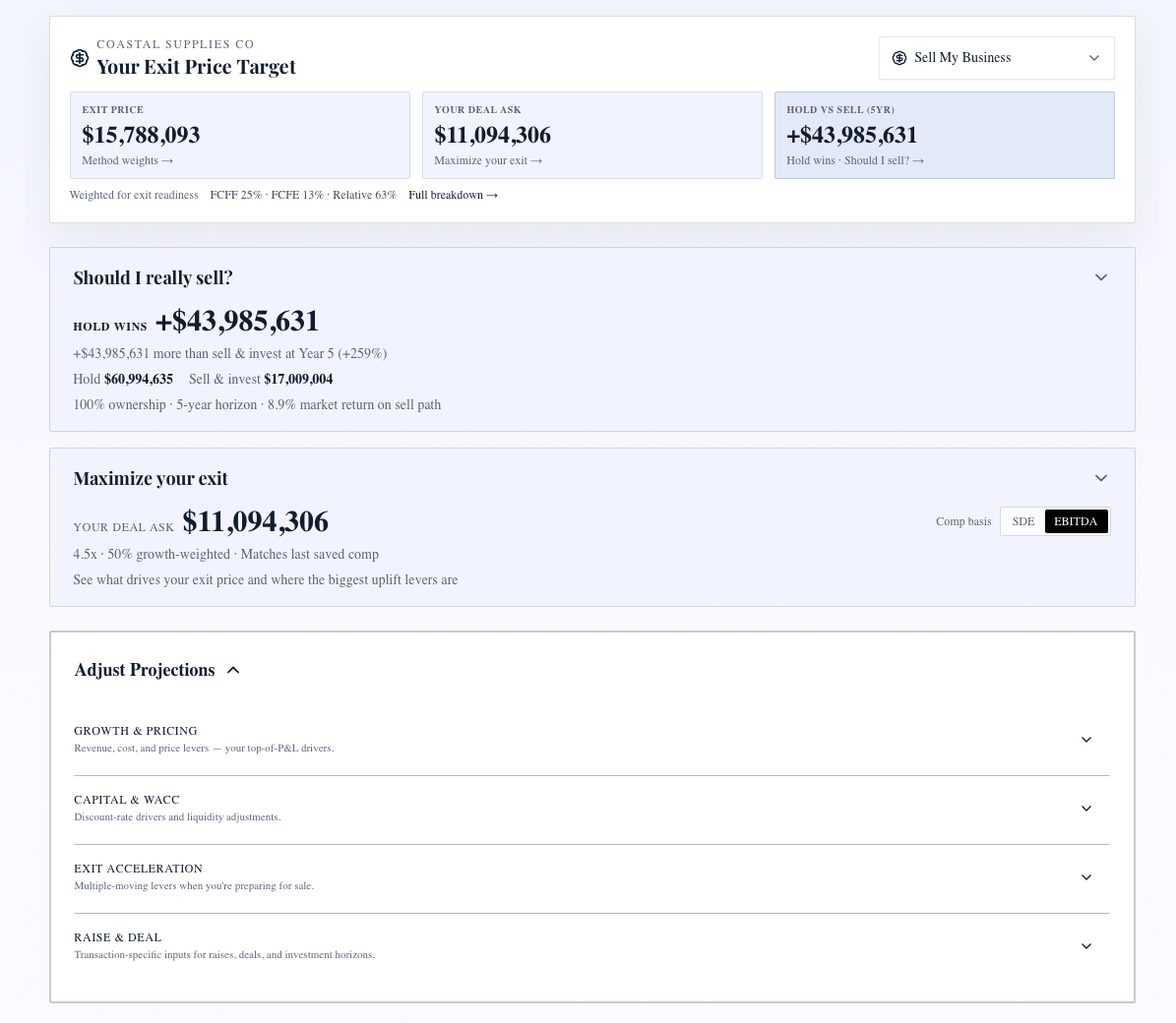

How to Value a SaaS Business: A Step-by-Step Framework

Knowing how to value a SaaS business is not a one-time exercise you complete before an exit. It is a discipline — a structured method of reading your own financial signals clearly enough to know which levers actually move the number a buyer, investor, or co-owner will ultimately pay. The process has five steps: clean the SaaS-specific metrics that general accounting does not surface, run three independent valuation lenses, and blend them into a defensible range you can explain and defend at a whiteboard. This guide walks through each step using the same methodology behind Exit Matters Chapters 4, 6, and 7.

Step 1: Normalize Your SaaS Metrics Before the Math Starts

Valuation math built on dirty inputs produces a number that collapses under diligence. Before opening a model, prepare four clean metrics.

Committed ARR. Annual recurring revenue should reflect only committed, recurring software contracts — no one-time setup fees, no professional services, no non-contractual usage overages. Convert every contract to its monthly equivalent and multiply by twelve. A customer on a $3,500 monthly plan contributes $42,000 ARR. A customer on a $36,000 annual contract billed upfront contributes $36,000 ARR — but if eight months remain on that contract, only the twelve-month annualized figure counts. Multi-year contracts follow the same logic: divide by contract length in years. The resulting ARR schedule should reconcile exactly to your billing system. If it cannot, a buyer's financial due diligence team will reconstruct it themselves and discount the result.

Net Revenue Retention (NRR). Measure NRR by comparing the ARR from a cohort of customers at the end of a twelve-month period to where that same cohort started, excluding any new customers acquired during that window. Above 100% means the existing base is growing through upgrades, seat additions, or cross-sells. Below 100% means you are losing ground on existing accounts before writing a single new contract. The current market places NRR above 110% as a clear premium driver on the 3.0× to 9.0× EV/EBITDA band; anything below 95% signals retention risk that compresses multiples materially.

Monthly gross churn. Calculate as ARR cancelled in the period divided by opening ARR. Below 0.5% monthly gross churn keeps you in premium territory. Above 1.5% monthly — roughly 18% annualized — the business begins to look structurally leaky. Monthly churn feeds directly into every forward projection in the FCFF model; a 1.0% monthly churn rate compounded over five years removes roughly 45% of today's revenue base before any growth is layered on top.

Owner-led revenue mix. Track what percentage of new ARR in the last twelve months required the founder personally on the close. Above 50% is a discount driver that affects every lens because it prices in key-person risk. Document the split from your CRM so the number is defensible, not estimated.

With these four inputs prepared, the downstream math is anchored to something real.

Step 2: Run Free Cash Flow to the Firm (FCFF)

FCFF is the unlevered approach — it values the enterprise on the cash flows the operations generate, independent of how the business is financed. For SaaS, the model requires four building blocks: a five-year revenue projection anchored to your clean ARR and a realistic growth assumption; an operating margin path that accounts for planned reinvestment in sales, product, and infrastructure; a terminal value at a conservative perpetual growth rate (typically 2–3%); and a weighted average cost of capital (WACC) that reflects the riskiness of those specific cash flows.

Choosing the right WACC is where most founders get lost. Private SaaS businesses with NRR above 100% and low customer concentration carry more predictable cash flows than cyclical service businesses, which justifies a WACC toward the lower end of the 12–20% range typical for companies this size. The Cost of Capital Simulator in XIT Matters builds the rate from component inputs — risk-free rate, equity risk premium, size premium, and a company-specific adjustment for concentration, retention quality, and owner dependence. Adjust any slider and the FCFF answer reprices instantly.

After discounting the projected cash flows back to today, apply an illiquidity discount. Private companies are harder to sell than publicly traded stocks — standard discounts run 20–35% depending on the size of the buyer pool, quality of documentation, and how transferable the business is without the founder. A $5M ARR SaaS with documented playbooks and predictable retention might justify 20–25%. A founder-dependent business with thin documentation sits at 30–35%.

The FCFF result is your intrinsic enterprise value — what the business is worth in isolation based on the cash it will generate. Think of it as the floor of rational value.

Step 3: Run Free Cash Flow to Equity (FCFE)

FCFE applies the same projection machinery but after debt service and net new borrowing. For bootstrapped SaaS businesses with clean balance sheets, FCFF and FCFE land close together. However, venture debt, revenue-based financing, or convertible notes on the cap table create a wedge — and buyers will find them during diligence whether you surface them first or not.

Running the FCFE lens explicitly makes the capital structure visible in the output rather than buried in a footnote. It also clarifies the equity value — the slice that belongs to founders and existing investors after all obligations are settled. Exit Matters Chapter 7 notes that founders who present a clean capital-structure summary alongside the valuation output signal diligence-readiness, which reduces buyer risk perception and supports the upper range of the multiple band during negotiation.

Step 4: Apply EV/EBITDA Market Comps

EV/EBITDA anchors enterprise value to what comparable transactions are actually paying in the current market. For SaaS businesses in the $1M–$25M ARR range, the 2026 band runs from a low of 3.0× through a median of 5.5× to a high of 9.0×.

Low end (3.0×) applies when NRR is below 100%, year-over-year ARR growth is under 20%, gross margin is below 65%, owner-led sales dominate, and top-customer concentration exceeds 25% of ARR. Each factor compounds: a buyer sees a leaky, founder-dependent business with thin economics and concentrated risk — and prices all of it in.

Median (5.5×) reflects a well-run SaaS with 25–35% ARR growth, NRR between 100% and 110%, gross margin above 70%, and a sales motion that functions without the founder on every deal. Most competently operated B2B SaaS businesses in this revenue range land near the median when financials are clean.

High end (9.0×) is reserved for businesses that clear all four premium thresholds at once: NRR above 110%, gross margin above 75%, monthly churn below 0.5%, and ARR above $2M with a rule-of-40 score above 40. These businesses demonstrate expanding economics, minimal founder dependency, and retention that compounds without requiring new sales to replace lost revenue. When all four characteristics converge, buyers are willing to pay a significant premium because the risk is structurally low and the growth is self-reinforcing.

What the Discount Drivers Mean in Practice

Top-customer concentration above 25% and owner-led sales above 50% do not each subtract a fractional turn in isolation — they compound. Together they can take a business that would otherwise merit 5.0× to 5.5× down to 3.5× or below, because a buyer is effectively pricing two correlated catastrophic risks: losing the top customer and losing the founder in close succession.

Tech debt belongs in this conversation. A codebase that only the founding engineer can navigate, infrastructure that has not been updated in three years, or the absence of automated testing — all of these translate to a post-close remediation budget that buyers price into their offer, either through a lower multiple or a purchase-price adjustment. Surface the tech debt proactively with a remediation plan. It is more credible than silence and more defensible than discovery.

The EV/EBITDA Market Comps feature in XIT Matters places your current metrics against this band in real time. At sub-$10M ARR where EBITDA is often near zero as the business reinvests in growth, it supplements the EV/EBITDA view with an ARR multiple as a cross-check so the market signal stays visible even when trailing margins are thin.

Step 5: Build the Blended View from Exit Matters Chapter 7

The three lenses — FCFF, FCFE, and EV/EBITDA — typically produce different numbers, and that is the point. The gap between them tells you something. When FCFF implies a meaningfully higher value than the EV/EBITDA comp, the business has a forward-growth narrative that the trailing EBITDA does not yet reflect. When EV/EBITDA sits above the FCFF answer, the market may be paying a premium your DCF assumptions are not capturing — often because buyers see synergies or a platform acquisition opportunity that inflates comp data.

Chapter 7 of Exit Matters describes the Blended View as a deliberate weighting of the three lenses, not a mechanical average. The appropriate weights depend on who is asking and why.

Weighting the Three Lenses for Your Situation

The Six Persona Views in XIT Matters set default weightings for six user types: the day-to-day operator, the capital raiser, the exit planner, the co-owner in a buyout negotiation, the due diligence reviewer, and the board or advisor view. An exit planner persona weights market comps more heavily and surfaces the high-end scenario prominently — the buyer's likely range is the most relevant anchor. A capital raiser persona weights forward cash flows more heavily because the fundraising narrative centers on growth trajectory, not trailing EBITDA.

Real-Time Slider Modeling lets you override the default weights manually. If a buyer has signaled they are primarily intrinsic-value-oriented, you can tilt toward the FCFF lens and present a range that reflects how they will model the business. If multiple strategic acquirers are circling, you can weight market comps more heavily to anchor conversations at a level that reflects competitive tension. This is not about gaming the number — it is about presenting the valuation in the language the audience is already using.

Chapter 7 is explicit that the value of the Blended View is not that it averages away disagreement. It is that working through the weighting forces you to understand why the three lenses diverge — and that understanding converts a valuation number into a negotiating position.

A Worked Example: $5M ARR Horizontal B2B SaaS

Consider a horizontal B2B SaaS business serving professional services firms — accounting practices, legal teams, and management consultancies — at $5M ARR, growing 28% year-over-year, NRR at 104%, gross margin at 74%, EBITDA margin at 11%, top customer at 19% of ARR, and the sales team independently closing roughly 65% of new bookings. Monthly churn is 0.7% — above the premium floor of 0.5% but below the discount threshold.

A single rule-of-thumb calculator applies the median 5.5× and returns $27.5M. That number is not wrong. It is incomplete.

Running all three lenses produces a more useful picture. The FCFF model — projecting growth fading from 28% to 12% over five years, a 3% terminal rate, and a WACC of 14% to reflect horizontal-market competitive intensity and modest owner dependence — lands at roughly $24M to $27M enterprise value. FCFE sits close; the balance sheet carries only a modest revenue-based financing facility, so the equity adjustment is minor. The EV/EBITDA lens at 5.5× on $2.75M of EBITDA implies approximately $15M — but this business has 74% gross margin and positive NRR, both pointing toward the upper portion of the band rather than the median. Stretching toward 6.5× to 7.0× produces a range of $17.9M to $19.3M.

The Blended View for an exit-planner persona — market-comp tilted — converges around $21M to $25M as the defensible range. The gap between the FCFF intrinsic answer ($24M–$27M) and the EV/EBITDA market answer ($17.9M–$19.3M) is the story: this business's growth trajectory and cash generation outpace what trailing EBITDA alone can communicate. A founder who shows a clear path from 11% EBITDA margin to 18% over 24 months — through pricing discipline, reduced customer acquisition cost, and expanded NRR — closes that gap materially. The AI Scenario Analyst can model exactly that bridge, showing the dollar impact on each lens at each margin checkpoint.

From a One-Time Calculation to a Quarterly Management Tool

The Blended Valuation Engine is not meant for the week before you take a call from an acquirer. It is meant for every quarter you are running the business. Connect your financials or enter twelve months of P&L and balance sheet; the engine normalizes ARR, calculates NRR from revenue cohort data if available, and runs all three lenses automatically. The SaaS-specific sliders — ARR growth rate, NRR, gross margin, top-customer concentration, owner-dependence percentage, and recurring-versus-services revenue mix — appear as live inputs. Adjust any one and every lens plus the Blended View reprices in real time.

The AI Scenario Analyst turns that into a planning tool. Ask what the valuation looks like if monthly churn drops from 0.7% to 0.4% through a new onboarding investment, or what happens if you raise prices 8% with 90% retention on the base, or what the number looks like in eighteen months if you hit $7M ARR with margins expanding toward 18%. Each question returns the dollar impact on FCFF, FCFE, EV/EBITDA, and the blended answer — grounded in your actual financials, not a generic ARR rule of thumb.

The objective is directional accuracy you can act on before the next board meeting, investor conversation, or strategic inquiry lands in your inbox. Exit Matters Chapter 3 frames this as the 80/20 principle of valuation: you do not need audit-grade precision monthly. You need to know which two or three operational levers move the number that matters — and then spend the next twelve months on those levers instead of everything else. For most SaaS businesses in the $1M to $25M ARR range, those levers are NRR, gross margin, and owner dependence. The math makes it visible. The habit of checking it regularly is what compounds into a meaningfully higher exit.

Grounded in the FCFF/FCFE/EV/EBITDA Blended View, SaaS metric normalization methodology, and the Four Forces framework from Exit Matters Chapters 3, 4, 6, and 7, and the author's experience building and exiting Performance Matters. All worked examples are composites drawn from real founder engagements to protect confidentiality while illustrating the decision framework.