The Best Way to Value a Business Without an Expensive Appraiser Is to Run the Same Methods They Do — Yourself

The best way to value a business without an expensive appraiser is not to skip method or settle for a single revenue multiple. It is to run the same three institutional methods a professional appraiser would run — Free Cash Flow to the Firm, Free Cash Flow to Equity, and EV/EBITDA — on your own financials, then blend them into one actionable number that shifts with your goal. That work, done in ten minutes on a platform built for owners, delivers the 80 percent directional accuracy you need for sale preparation, negotiation, and everyday decisions at a fraction of the cost and time of a formal engagement.

Exit Matters Chapter 3 makes the case plainly: 80 percent of the results come from 20 percent of the inputs. A certified appraisal typically costs $5,000 to $25,000 for a small business and takes four to twelve weeks. A Quality of Earnings report tied to a transaction can run $50,000 to $200,000. The remaining 20 percent of precision — the immaculate adjustments, footnoted add-backs, and signed fairness opinion — rarely changes the decision in front of you. It just drains time and wallet while value slips away. The four-lens framework gives you 80 percent or more of the directional accuracy at roughly 2 percent of the cost and in a fraction of the time. Use the formal appraisal when the stakes are binding. Use the self-served institutional stack for everything else.

Why Formal Appraisals Cost So Much and Take So Long — and When You Still Need One

A licensed appraiser must produce a written report that can withstand scrutiny in court, before the IRS, or in a shareholder dispute. That requires deep diligence, comparable transaction research, multiple valuation approaches cross-checked, sensitivity tables, and a signed opinion letter. The process is deliberately rigorous because the document may become evidence.

You need that rigor for binding events: litigation, divorce settlements, IRS estate or gift tax filings, lender-required Quality of Earnings at close, or adversarial partner buyouts. In those cases a self-served range is not a substitute — it is preparation. You walk into the formal engagement with your own defensible numbers already in hand, so the conversation starts from a position of knowledge rather than blind trust.

For sale preparation and negotiation, however, the formal document is usually overkill until the very end. Sophisticated buyers expect to see seller-prepared models. They respect real methodology — three independent methods that converge on a range — far more than a single multiplier pulled from a public database. Lenders for most SBA or asset-based facilities will still require the CPA opinion at closing, but they are perfectly comfortable discussing terms against your own three-method analysis long before that stage.

The Three Institutional Methods You Can Run Yourself in Ten Minutes

The platform that delivers the best way to value a business without an expensive appraiser simply automates what the book teaches in Chapters 4, 5, 6, and 7.

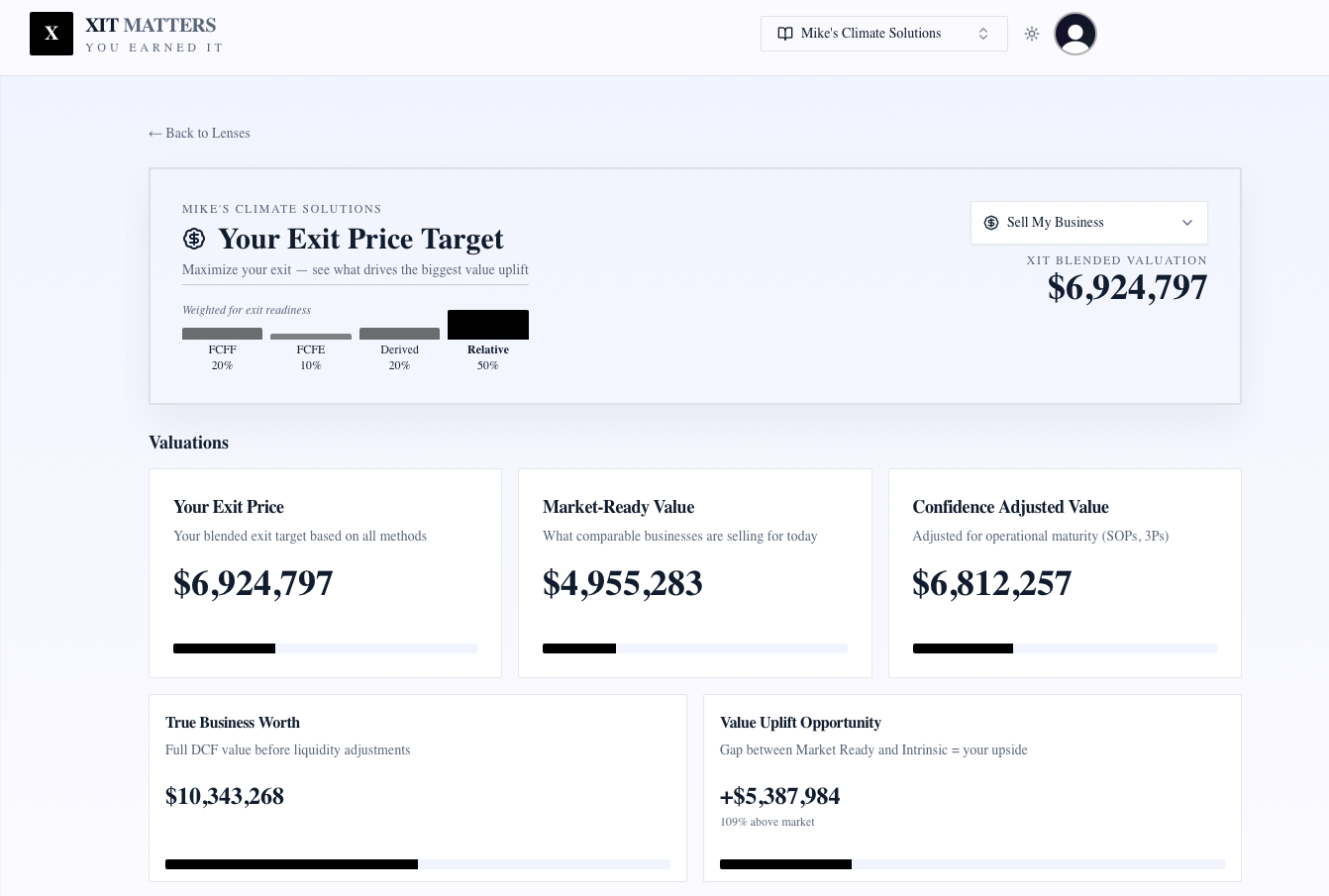

Free Cash Flow to the Firm (FCFF) — Lens 1, Cash Flow to the Business — calculates what the operations generate for all stakeholders before financing. You normalize EBITDA, subtract taxes as if unlevered, add back non-cash charges, subtract required reinvestment in equipment and working capital, project forward five years with realistic growth and terminal value, discount at your weighted average cost of capital, and apply an illiquidity discount. The result is the intrinsic enterprise value of the machine itself. Exit Matters Chapter 3 shows how the 80/20 Rule prunes unnecessary complexity here: most owners can ignore lease capitalization, minor R&D amortization, and every last owner perk without flipping the decision. Mike’s first rough valuation using unadjusted QuickBooks exports landed within 2 percent of the “perfect” version that cost weeks and thousands more. Direction stayed the same; the decision did not change.

Free Cash Flow to Equity (FCFE) — Lens 2, Cash Flow to the Owner — starts from the same cash flows but subtracts actual debt service and adjusts for net borrowing. It answers the more personal question: what cash is truly available to you after the bank and the tax man have taken their share? For owners preparing to sell, this lens often becomes the floor beneath any acceptable offer. It forces you to confront net debt, excess cash, and the real equity you would walk away with — numbers that matter far more in a negotiation than enterprise value alone.

EV/EBITDA — Lens 3, What Buyers Will Pay — applies a market multiple drawn from comparable transactions to your normalized EBITDA, then adjusts for the specific strengths and risks of your business: customer concentration, recurring revenue, owner dependence, growth trajectory, and capital intensity. The multiple is not a lookup table; it is a conversation with the data about how the market is currently pricing businesses like yours. Chapter 3’s 80/20 lens applies here too: thin transaction comps or unusual capital structure widen the range, which the platform flags so you know where to dig deeper before you sit down with a buyer.

None of this requires a PhD or a $25,000 engagement letter. Connect your financials or enter the last twelve months of P&L and balance sheet, and the engine produces all three numbers plus the default Blended View in roughly ten minutes. Change any assumption and the entire stack recalculates instantly — exactly what you need when you are stress-testing an offer or modeling different exit scenarios. The same 80/20 discipline that keeps the model fast also keeps it honest: if adding a complexity shifts the Blended View by less than 10–15 percent, the book advises you to drop it and move on.

The Blended View Becomes Your Real-Time Negotiation Anchor

Exit Matters Chapter 11 shows how owners who know their number in real time negotiate from strength instead of fear. The Blended View — Lens 4 — is the single number that combines the three methods with weights that shift depending on the conversation.

When you are preparing to sell, you reweight toward Lens 3 so the number reflects what a buyer is most likely to anchor on. When you are modeling your personal walk-away or negotiating with a lender, you tilt toward Lens 2. When you are evaluating operational improvements that will make the business more valuable to the next owner, Lens 1 carries more weight.

Mike, the composite HVAC owner in the book, used exactly this approach in four negotiations in a single quarter: a parts supplier demanding an 8 percent price increase, a large customer threatening to leave, a bank refinance, and a key employee asking for a raise. In each case he walked in with his Blended View and one supporting lens printed on a single page. He did not raise his voice or threaten to walk away. He simply stated the math: “An 8 percent increase hits my valuation by $130,000 over the planning horizon. I have run the numbers three ways. Can we find a middle path?” The supplier settled at 2.5 percent and protected $95,000 of value. The same pattern worked with the customer, the bank, and the employee.

Sale negotiations are no different. When you know your three-method range and can explain how you arrived at it, the conversation shifts from “what will you take?” to “here is the math behind my number.” Buyers respect owners who understand their own value drivers. It removes emotion from both sides of the table and replaces it with data that is hard to argue with.

Head-to-Head: Why the Self-Served Institutional Stack Beats the Alternatives for Most Owners

The comparison table above makes the trade-offs concrete.

A traditional appraiser delivers the full methodological stack and a binding document when you need one, but at $5,000 to $25,000 and four to eight weeks for a standard valuation — or $50,000 to $200,000 and longer for a Quality of Earnings tied to a transaction. That timeline and cost make sense only when the document must survive adversarial scrutiny.

A generic calculator is fast and free or cheap, but it stops at a single revenue or EBITDA multiple. It cannot show you the impact of working-capital changes, cannot reweight for different negotiation contexts, and carries zero credibility when a buyer or lender asks how you arrived at your number. It is a starting guess, not a defensible range.

The self-served institutional platform sits in the only quadrant that gives you real methodology, live recalculation as your data or assumptions change, and a Blended View you can actually use in conversation — all for free during the public beta and in ten minutes. Beta users are grandfathered when paid plans launch, so the window to put the full stack to work without budget approval is open now.

Accuracy You Can Actually Use: 80/20 Directional Accuracy for Real Decisions

For an owner running clean financials, the three-method blended answer typically lands within 10 to 20 percent of a later CPA-issued range. That variance is not a flaw; it is the 80/20 Rule in action. The last 20 percent of precision rarely flips the decision, but it always costs time and money. The platform surfaces low-confidence inputs — unusual working-capital swings, thin comparable data, or heavy owner add-backs — so you know exactly which assumptions to firm up before you sit down with a buyer or a formal appraiser.

Messy books widen the gap, which is why the first step is usually a quick normalization pass rather than a forensic audit. The goal is not to replace your CPA. The goal is to stop waiting for the CPA’s sign-off before you make the decisions that actually move value.

Get Your Defensible Range Before You Spend a Dime — and Use It

The best way to value a business without an expensive appraiser is to run the institutional stack yourself first. Connect your financials or upload the last twelve months, receive the three-method range plus Blended View in ten minutes, and immediately begin using that number as your negotiation anchor and decision compass. Re-run it after every material change — a new customer, a price adjustment, a working-capital improvement — and watch the range tighten or shift in real time.

When a binding event arrives, you already have the defensible range in hand. You walk into the formal appraisal or the buyer’s due diligence room prepared rather than blind. The 80/20 alternative — institutional method first, formal opinion only when required — saves most owners between $40,000 and $180,000 while giving them a number they can actually use every week leading up to the exit.

That is the difference between guessing what your business is worth and knowing what it is worth, with the math to back it up.

Grounded in the 80/20 Rule, four-lens framework, FCFF/FCFE/EV/EBITDA math, and negotiation-anchor examples from Exit Matters Chapters 3, 11, and the Appendix. All case examples are composites drawn from real owner engagements to protect confidentiality while illustrating the decision framework.