How to value a contracting business — why project shops need three-method math

Applying a single revenue or EBITDA multiple to a contracting company ignores the mechanics that actually drive transaction price. Work-in-progress accounting, warranty and callback reserves, bonding capacity, and the split between recurring service agreements and one-time construction projects determine whether a buyer prices you at 2.5× or 5.5×. Learning how to value a contracting business means normalizing EBITDA to true free cash flow, running FCFF, FCFE, and EV/EBITDA together, and reading the transaction band against the premium and discount drivers that govern specialty contractor deals in 2026.

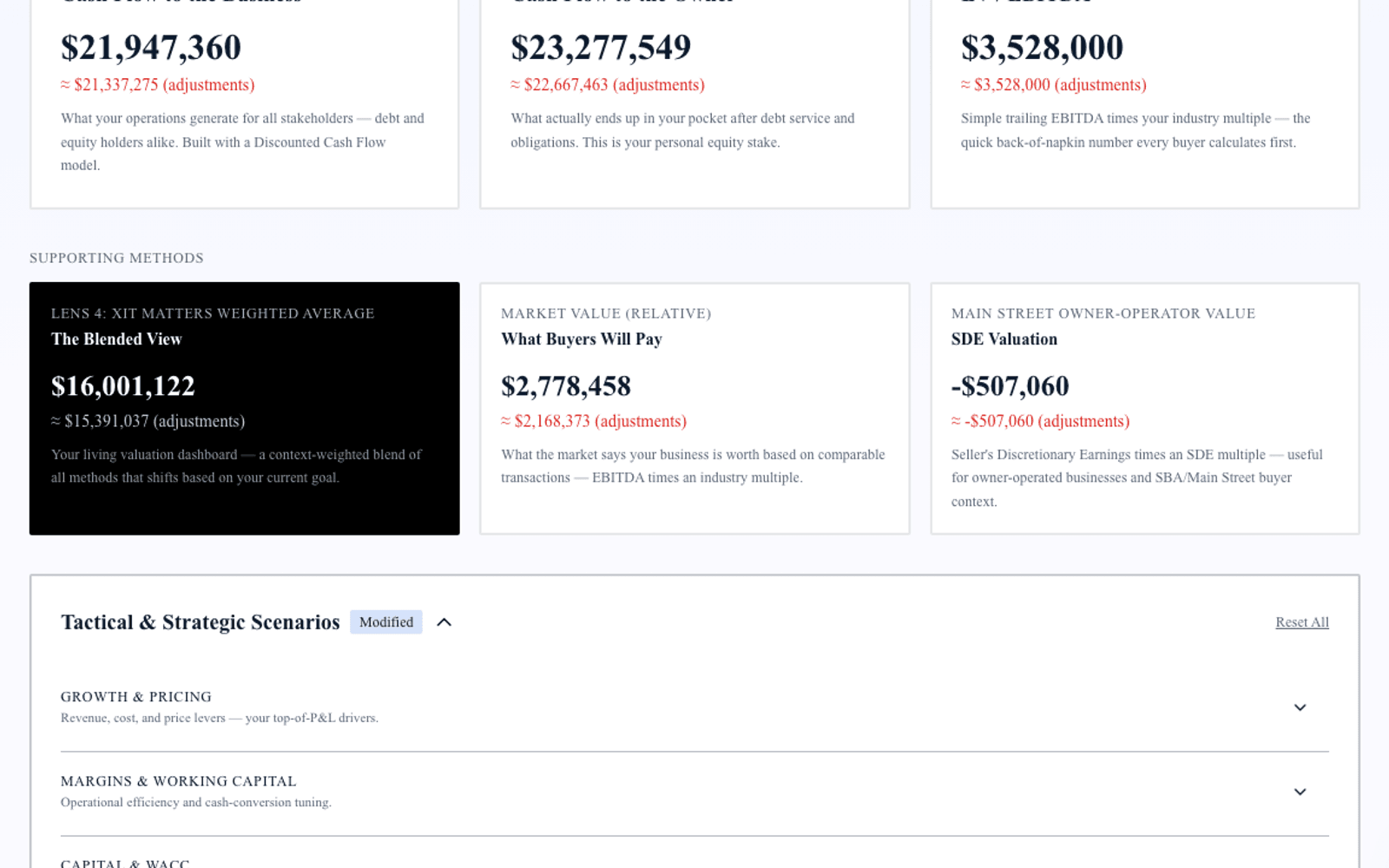

Exit Matters Chapter 7 describes the Blended View — three institutional methods weighted toward the decision in front of you. Contracting adds four complications generic guides skip: percentage-of-completion revenue timing, service versus project revenue mix, bonded crew bench and licensing, and GC or commercial customer concentration. Handle those correctly and standard cash-flow logic applies.

The typical contracting business that transacts in the SMB market runs $1M–$20M in revenue and produces normalized EBITDA between $200K and $3M. Band position — not headline EBITDA — determines acquirer pricing.

Step 1 — Normalize EBITDA for a contracting business

Add back to reach gross normalized EBITDA:

Owner compensation above or below market-rate operations manager or project executive pay. One-time tool, vehicle, or equipment purchases expensed through the P&L. Non-recurring warranty settlements, legal claims, or project write-offs that will not repeat. Depreciation and amortization. Related-party rent or vehicle charges above or below arm's-length rates.

Subtract to arrive at net normalized EBITDA:

Maintenance capex on vehicles, tools, and equipment required to maintain current bid capacity. Normalize percentage-of-completion timing — if you recognized revenue early on a $2M job still 40 percent complete, buyers will restate. Separate service-agreement revenue from new-construction and renovation project revenue in your presentation.

The result is Normalized EBITDA after Maintenance Capex — the foundation for FCFF and EV/EBITDA.

Step 2 — FCFF for contractors (the enterprise lens)

FCFF = Normalized EBITDA after Maintenance Capex × (1 − effective tax rate) + non-cash charges − net working capital investment − growth capex

Working capital in contracting is material. Unbilled revenue, retainage receivable, and WIP inventory tie cash while suppliers and subs expect payment on 30-day terms. A contractor running 48 days sales outstanding with heavy retainage has fundamentally different FCFF than one billing monthly on service agreements with 22-day DSO.

Growth capex — additional trucks, expanded shop, new trade licenses — is discretionary above maintenance. Model separately for buyers evaluating expansion capacity.

Discount rates for private contractors typically run 13–20 percent depending on project mix, concentration, and owner dependency. Specialty trades with recurring service revenue justify the lower end; general contractors with lumpy backlog justify the upper end.

Step 3 — FCFE and equity walk-away

FCFE = FCFF − interest expense × (1 − tax rate) + net debt issuance

Contracting firms carry vehicle fleets, equipment loans, and lines of credit tied to WIP. Enterprise value minus net debt equals equity walk-away. A contractor with $3.1M enterprise value and $520K net debt receives $2.58M at wire — not $3.1M.

FCFE also informs reinvestment: if annual equity free cash flow is $280K on $1.4M equity value, that 20% return competes with adding a service territory or holding for a strategic sale.

Step 4 — EV/EBITDA market anchor for contracting

| Position | Multiple |

|---|---|

| Low (discount) | 2.5× |

| Median | 3.8× |

| High (premium) | 5.5× |

Premium placement requires three or more of:

Service contracts and recurring maintenance above 50 percent of revenue. Bonded and licensed crew bench with documented safety and training programs. Commercial customer mix with assignable agreements. Backlog visibility beyond twelve months on signed contracts. Project management infrastructure that operates without the owner on every bid.

Discount placement results from:

Owner as lead estimator and project manager on all major jobs. Single GC or commercial customer above 35 percent of revenue. Lumpy project revenue without service anchor. Warranty and callback history above industry norms.

At 3.8× median on $720K normalized EBITDA, enterprise value lands at $2.74M. At 5.5× for a premium HVAC operator with 62 percent service-agreement revenue, enterprise value reaches $3.96M.

Step 5 — Blended View for contracting owners

Weight FCFF heavily for operating and reinvestment decisions — can you fund a second crew from cash flow? Weight EV/EBITDA heavily when preparing to sell to a strategic acquirer or PE platform. Weight FCFE when evaluating personal walk-away after equipment debt.

Run all three. Convergence within 15–20 percent signals a defensible range; divergence above 40 percent usually reveals WIP normalization issues, unpriced warranty reserves, or multiple assumptions misaligned with comparables.

Specialty trade premiums — why HVAC, electrical, and plumbing trade higher

General contractors and residential builders compress toward the discount end of the 2.5×–5.5× band because completion risk, warranty exposure, and GC concentration dominate buyer models. Specialty contractors with licensed trades, service-agreement revenue, and commercial maintenance contracts structurally trade higher within the same band.

An HVAC operator with 61 percent service-agreement revenue and NATE-certified technicians supports median-to-premium placement because cash flow resembles a subscription business more than a project shop. An electrical contractor with bonded commercial service contracts and documented safety programs trades similarly. A general contractor bidding custom homes with 70 percent project revenue and the owner on every estimate sits at 2.8×–3.2× regardless of strong gross margin.

When you model how to value a contracting business, identify your trade category honestly. Specialty service-heavy operators should anchor comparables to mechanical and trade roll-ups; project-heavy GCs should anchor to construction services comps with explicit completion and warranty reserves in FCFF.

Percentage-of-completion and billing timing

Contractors on accrual accounting recognize revenue as jobs progress. Timing differences between cost incurrence, billing milestones, and cash collection create FCFF volatility that trailing EBITDA alone obscures. A contractor who billed 85 percent on a job that is 60 percent complete shows inflated trailing EBITDA; one who under-billed a 90-percent-complete job shows depressed EBITDA.

Normalize open jobs before valuation: list contract value, costs incurred, percent complete by cost, billed to date, and retainage held. Buyers rebuild EBITDA from job schedules, not tax returns alone. Presenting a clean WIP schedule before market removes the most common QoE surprise in contractor diligence and tightens the spread between FCFF and EV/EBITDA in the Blended View.

Bonding, WIP, and warranty — three adjustments buyers always make

1. Work-in-progress and retainage schedules. Buyers reconcile job costs, percent complete, and billing status on every open contract. Present a WIP schedule with job names, contract value, costs to date, and billed-to-date before diligence starts.

2. Warranty and callback reserves. Mechanical and specialty trades carry post-completion liability. A firm with 4 percent of revenue in callbacks over three years receives EBITDA adjustments; one with documented QA and sub-1 percent callback rates supports premium placement.

3. Bonding and license transferability. Surety bonding capacity often rests on owner personal indemnity and experience. Ownership change triggers surety review; document licensed journeymen, safety record, and backlog assignability to reduce close risk.

4. Subcontractor dependency. Heavy reliance on unbonded subs for core trade work creates execution risk that compresses FCFF discount rates. In-house crew capacity is premium-band evidence.

How XIT Matters handles contracting valuation

XIT Matters runs FCFF, FCFE, and EV/EBITDA simultaneously with the contracting band (2.5× / 3.8× / 5.5×) and premium/discount drivers pre-loaded. Real-Time Slider Modeling adjusts service-contract mix, customer concentration, and maintenance capex with instant recalculation across all three methods.

The AI Scenario Analyst answers compound questions: "What if we grow service agreements from 44% to 60% of revenue over two years?" Six Persona Views cover seller, operator, and capital-raiser contexts. QuickBooks and Xero compatible. Free during beta.

Worked example — $6.8M mechanical contractor

Revenue $6.8M, gross normalized EBITDA $920K, maintenance capex $95K, net normalized EBITDA $825K. Net debt $410K. Service agreements 56 percent of revenue; owner still estimates jobs above $75K but two project managers run field operations.

FCFF: Discounted at 14.8% WACC: intrinsic enterprise value $3.4M–$3.9M.

FCFE: Equity walk-away after $410K net debt: $2.7M–$3.2M.

EV/EBITDA: $825K × 3.8× = $3.14M median; 4.6× premium scenario = $3.80M.

Blended seller range: $3.2M–$3.7M enterprise; $2.8M–$3.3M equity after debt. Delegating estimating on jobs below $100K and documenting PM authority six months before sale moves the blend toward premium without adding current-year EBITDA.

Preparing contractor financials for buyer diligence

Buyers and QoE teams request a consistent document package: three years tax returns or reviewed financials, trailing-twelve-month job-cost detail, open WIP schedule with retainage, service-agreement customer list with contract values and renewal dates, equipment and vehicle fleet list with ages and liens, insurance and bonding history for three years, and warranty or callback log by job type. Assembling this before market shortens diligence by weeks and prevents the EBITDA restatements that collapse LOI price.

Normalize owner compensation to a market-rate operations executive in the financials you present — not zero, not $400K on a $900K EBITDA shop. Buyers restate unrealistic owner comp in both directions. Present maintenance capex as a separate line from growth capex so FCFF baseline is defensible. If you carry significant related-party rent or vehicle leases, disclose and normalize before the first buyer call rather than discovering adjustments in week three of diligence.

When to escalate to formal contracting appraisal

Engage CPA-led Quality of Earnings or formal appraisal for signed LOI diligence, SBA-backed acquisitions, partnership buyouts with adversarial parties, and estate or litigation contexts. Bond underwriters may require third-party validation when ownership change affects bonding capacity above certain thresholds. The blended three-method baseline gets you to those conversations prepared — WIP normalized, service mix documented, multiple band position understood.

Subcontractor versus in-house labor mix also affects band placement. A mechanical contractor self-performing 80 percent of install labor with journeyman bench depth supports premium EV/EBITDA; a firm subcontracting 70 percent of field work carries margin risk and execution discount that compresses FCFF discount rates. Document crew certifications, safety EMR, and in-house versus sub hours by job type before buyer diligence — these operational details move multiples as much as headline EBITDA.

Retainage held on commercial contracts is the other working-capital item contractors overlook. Ten percent retainage on a $2M open contract ties $200K until final completion — cash you earned but cannot spend. Buyers model retainage release schedules in FCFF year one through year three; presenting retainage by job with expected release dates prevents conservative buyer assumptions that undervalue near-term cash generation.

Bottom line

How to value a contracting business in 2026 requires normalizing EBITDA after maintenance capex and WIP timing, running FCFF and FCFE for enterprise and equity views, applying the 2.5×–5.5× band with explicit service-mix and concentration drivers, and blending all three toward your decision. XIT Matters automates that framework — contracting band loaded, concentration and service sliders built in — free during beta. Ten minutes to your first answer, then model the moves that shift you from discount to median before the acquirer arrives with their own spreadsheet.