How to Value an Agency Business the Right Way in 2026

If you are learning how to value an agency business, the most important thing to understand upfront is that agencies are among the most volatile businesses to price — and the most mispriced. Two agencies with identical revenue and nearly identical profit margins can trade at 2.5× and 6.0× EBITDA respectively, and both numbers are correct. The spread is not a mistake. It reflects the things the income statement cannot show: how much of that revenue recurs monthly, whether the founder is the only person buyers and clients trust, and whether the client base is spread across multiple industries or concentrated in one sector that could cycle.

Generic business broker multiples and revenue-based rules of thumb collapse the moment an agency has any real complexity. The only reliable path is the same three-method institutional approach that sophisticated acquirers and PE-backed rollup platforms use: Free Cash Flow to the Firm for intrinsic cash-flow value, Free Cash Flow to Equity for what your ownership stake is actually worth after obligations, and EV/EBITDA anchored against what the 2026 market is paying for comparable agencies. For SMBs in the $1M to $15M revenue range, the agency band sits at approximately 2.5× on the low end, 4.0× at the median, and 6.5× at the premium. The methods tell you where in that band your specific business belongs — and exactly which levers move it.

Step One: Normalize Earnings Before Any Method Touches the Numbers

The first substantive step in how to value an agency business is always earnings normalization. This is where most owners — and many brokers — introduce the largest errors.

Agency income statements almost always contain: owner compensation above market rate (common in profitable S-corps and LLCs), personal vehicle and travel expenses run through the business, non-recurring project revenue that inflated one specific year, and sometimes inflated agency fees paid to a related entity the owner controls. Each of those items needs to be adjusted before running any valuation method, because the three lenses operate on earnings quality — not the number your accountant prints on a Schedule C.

Owner compensation normalization deserves particular care. If you paid yourself $350,000 last year and a replacement CEO for your agency would cost $175,000 on the open market, the $175,000 difference is a legitimate add-back. But if you run a ten-person shop and your replacement would realistically cost $200,000, you are only adding back $150,000. Be precise rather than generous — buyers will rebuild the number in diligence and if your normalized EBITDA does not survive that rebuild, the deal chips at LOI.

Revenue normalization matters equally. A project that brought in $400,000 in one calendar year but is non-recurring should be flagged and removed or haircut in the trailing twelve-month calculation. Buyers are normalizing to a sustainable run-rate, not your best year. If the project was truly one-time, it inflates your EV/EBITDA base without improving your multiple — and sophisticated buyers will see through it immediately.

Once earnings are clean, normalize to trailing twelve months and, if your revenue has been growing steadily, prepare a forward look as well. The FCFF method in particular benefits from a five-year projection anchored on a defensible normalized base.

Step Two: Understand the Agency Multiple Band — 2.5× to 6.5×

The 2026 agency EV/EBITDA band for SMBs running $1M to $15M in revenue clusters into three positions based on the drivers buyers and investors actually underwrite.

Low end (2.5×–3.0×). Project-revenue-heavy shops where the majority of top-line is non-recurring. Owner is the primary rainmaker and key client relationships report to the founder personally. Client base concentrated in one or two industries. Team is capable but not empowered to win new business independently. Buyers price in the risk that revenue walks out the door with the founder.

Median (3.5×–4.5×). Meaningful retainer base — typically 40–60 percent of revenue under month-to-month or annual contracts. Some leadership depth: an account director, project manager, or operations lead who can run the business without the founder in the building for thirty days. Client base spread across two to four verticals. Documented SOPs for delivery. These agencies attract financial buyers and strategic acquirers without heroic assumptions about what happens post-close.

Premium (5.5×–6.5×). Productized service model where deliverables are packaged, scoped, and priced consistently. Retainer revenue above 60 percent of trailing twelve months. Senior leadership team with documented tenure and client retention records. No single client above 20 percent of revenue. Multi-vertical client base. The founder can step back without a measurable revenue impact. These agencies attract platform add-on interest from PE-backed rollups and command premium because buyers underwrite continuity, not hope.

Your position within the band is not fixed. It is a function of choices you make over the next twelve to twenty-four months — and the scenario tools in a proper valuation engine let you quantify those choices in dollars before you spend on them.

Step Three: Run the Three Institutional Methods on Your Agency Financials

Once earnings are normalized and you understand where you sit in the band, the three methods give you three complementary views of what your agency is actually worth.

Free Cash Flow to the Firm (FCFF) measures the cash the agency operations generate for all capital providers, independent of how the business is financed. Start with normalized EBITDA, subtract taxes as if the agency were unlevered, add back non-cash charges like depreciation on owned equipment or amortization of any prior acquisition goodwill, and subtract the reinvestment required to sustain the business. For most agencies reinvestment is modest — some software tooling, periodic hardware, and the working-capital needs of a growing retainer base — but it is never zero. Project the resulting cash flows forward five years using a defensible growth assumption, apply a discount rate that reflects the agency's actual risk profile (including the key-person and concentration risks discussed above), and discount back to present value with an illiquidity adjustment appropriate for a private business of this size. The result is the intrinsic value of the agency's operations — what the cash-flow machine is worth independent of what any specific buyer is willing to pay today.

Free Cash Flow to Equity (FCFE) answers the more personal question: what cash actually flows to your equity stake after every obligation is met? For agencies this means subtracting debt service on any business line of credit, equipment loans, or SBA obligations from FCFF. Agencies are generally asset-light and many carry minimal debt — but if you took on an SBA loan to fund a prior acquisition or build out office space, FCFE will be meaningfully lower than enterprise value implies. FCFE is the number that tells you what your ownership stake actually delivers in cash terms if you hold the business rather than sell it. It is also the lens that catches the hidden cost of rapid growth: an agency growing 30 percent per year may show strong EBITDA but weak FCFE because working-capital demands — project receivables, payroll ahead of collections — consume the apparent profit. Running FCFE alongside FCFF prevents that kind of growth-story illusion from inflating your exit expectations.

EV/EBITDA is the market lens — what comparable agency transactions are actually pricing at in 2026. Apply the appropriate multiple from the band to your normalized trailing twelve-month EBITDA, adjust for the premium and discount factors that move you within the range, and the result is enterprise value from a market-comparable perspective. This is the number most brokers and strategic buyers will anchor conversations around, which is precisely why you need the other two methods to validate or challenge it. A multiple that looks high relative to your FCFF — because your EBITDA margins are strong but growth is decelerating — is a signal to negotiate carefully rather than accept the first offer.

Step Four: Retainer Mix Is the Dominant Multiple Driver — Model It Explicitly

Of all the drivers that move an agency within the 2.5×–6.5× band, retainer concentration is the single most powerful. It deserves its own step.

Buyers and strategic acquirers treat retainer-heavy agencies differently at a structural level because the revenue profile resembles a subscription business: predictable monthly cash, low renewal cost relative to new-client acquisition, and resilience across economic cycles when clients are locked into scopes that deliver ongoing value. Above 60 percent retainer mix, buyers begin applying SaaS-adjacent reasoning to the multiple — and that reasoning lives closer to 6× than to 3×.

Below 40 percent retainer revenue, the agency is underwriting against project pipeline, which is inherently uncertain and requires constant sales effort to replace. Buyers discount for that uncertainty because they cannot model the next twelve months with confidence. The same agency with identical EBITDA but 35 percent retainer mix versus 65 percent retainer mix may trade at a 1.5×–2.0× spread in multiple — a difference of millions of dollars on a $5M EBITDA business.

The practical path to improving retainer concentration starts with your existing project clients. Which relationships are large enough and strategic enough that the client would benefit from a defined monthly scope? Converting even two or three high-value project relationships to quarterly-renewing retainers shifts the mix measurably. Track renewal cycles, document the renewal conversations, and build at least two full renewal cycles of documented history before claiming the revenue as genuinely recurring in a valuation conversation.

Step Five: Quantify the Owner Rainmaker Discount and Model the Fix

The owner rainmaker discount is the second largest single-point driver in agency valuation — and the most common reason a well-run agency trades at the low end of the band rather than the median or premium.

When the founder is the primary — or only — business-development engine, buyers underwrite a fundamental continuity risk. If the owner departs or steps back meaningfully post-close, will clients stay? Will the pipeline refill? The honest answer in a rainmaker-dependent agency is often no, or at least not reliably, and buyers price that risk into the deal through a lower multiple, a larger earnout tied to post-close revenue, or a longer tie-in period for the founder. All of those structures reduce effective deal proceeds.

The documented fix is a proven account director, business-development lead, or senior partner who has independently renewed or grown client relationships for at least twelve months before the valuation conversation. Ninety days of tenure does not move the needle. Two renewal cycles — where the new hire, not the founder, owns the client relationship — is the threshold buyers need to price out the key-person discount.

Model this before committing to the hire. Run the scenario: what is your blended valuation today with the rainmaker discount applied versus what it would be with a proven account director in seat for eighteen months? The delta in dollars is the maximum rational budget for that hire. In most agencies in the $2M–$10M revenue range, the valuation lift from credibly removing the rainmaker dependency exceeds three to five years of the hire's salary.

Step Six: Apply the Blended View to Get a Decision Compass

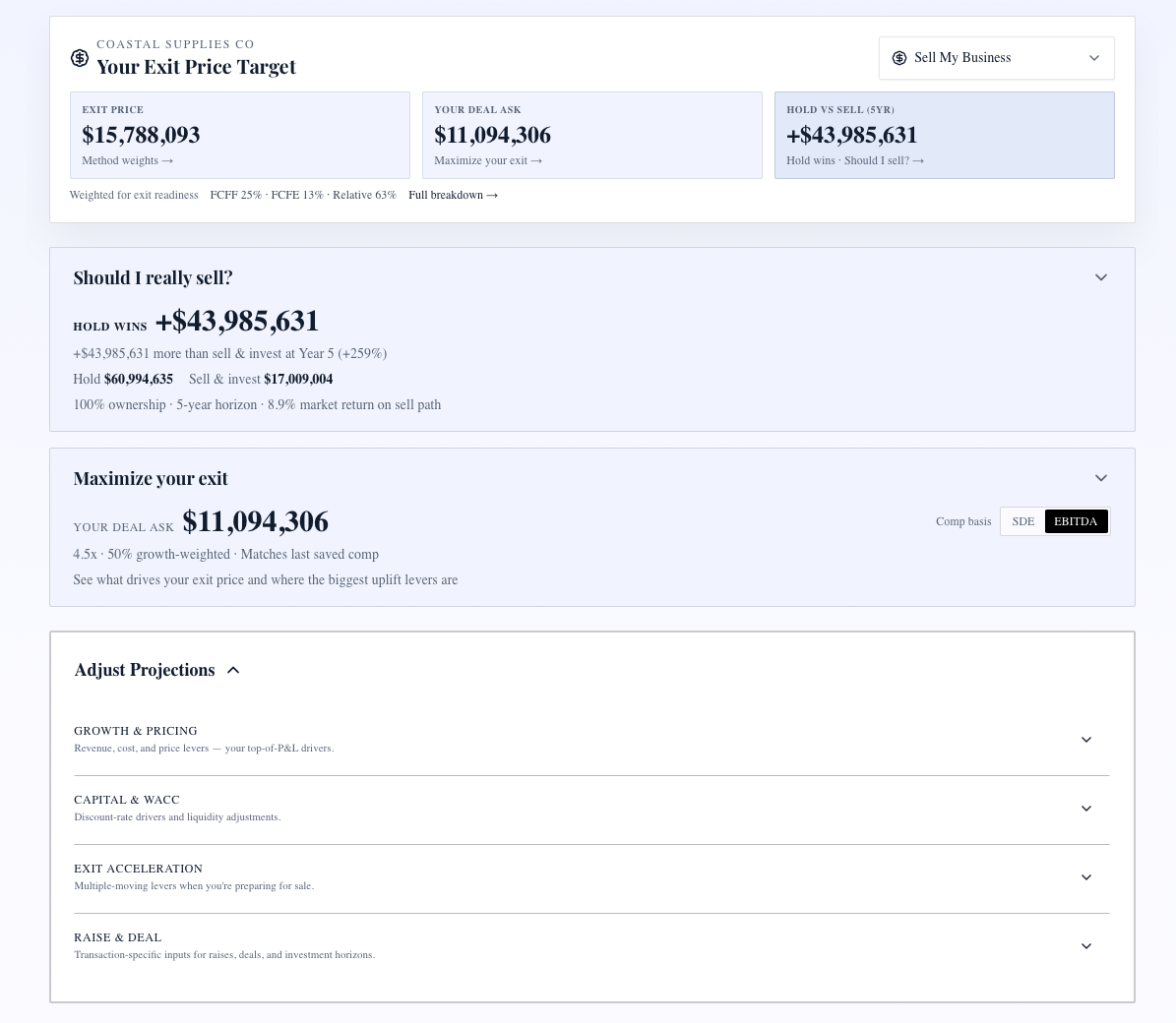

Three methods, three numbers — the Blended View turns them into a single defensible range that shifts depending on what decision you are actually making.

If you are managing the agency as a going concern and optimizing for growth, the default blend weights the cash-flow lenses more heavily: roughly 40 percent FCFF, 40 percent FCFE, 20 percent EV/EBITDA. The operational machine is what you are managing — your cash-flow quality and equity yield are the primary signals.

If you are preparing for a sale in the next twelve to twenty-four months, the weights shift toward what buyers will pay: 20 percent FCFF, 20 percent FCFE, 60 percent EV/EBITDA. The market lens becomes dominant because the transaction will price on the multiple, and the other methods validate or flag risk in how the market number was derived.

The same agency can show a Blended View of $3.4 million under owner-weighting and $4.1 million under pre-sale weighting with identical financials. That spread tells you exactly how much value is accessible if you shift from managing for retained earnings to managing for exit. XIT Matters recalculates the Blended View instantly as you change persona weights, update financial inputs, or move scenario sliders — so the decision compass stays live rather than being a one-time snapshot.

The Agency Levers That Actually Move the Number

Once the four-lens framework is clear, the highest-leverage moves are obvious.

Retainer conversion is the largest multiple lever. Target your three to five most stable project clients and design a recurring scope — strategy retainer, monthly reporting and optimization, fractional leadership — that translates project work into committed monthly revenue. One converted anchor client at $20,000 per month changes the retainer percentage of a $2M agency by twelve points, which can move the EV/EBITDA multiple by a half turn or more.

Leadership bench depth removes the rainmaker discount. Every month an account director independently manages and renews a client relationship, the key-person risk evidence accumulates. Document retention rates under the new structure — not just anecdotally, but with renewal records and a client-relationship ownership map that makes the bench depth visible in diligence.

Vertical diversification reduces concentration risk. When no single industry makes up more than 25–30 percent of revenue, the business is resilient to sector cycles and far more attractive to buyers who cannot afford to underwrite sector exposure. New business targeting in underrepresented verticals — even one or two new client wins per quarter — shifts the mix over eighteen months without disrupting existing relationships.

Productized delivery lifts margins and repeatability simultaneously. When core services are scoped and delivered through a documented methodology rather than bespoke from scratch every engagement, gross margins improve, onboarding accelerates, and buyers can model the cost structure with confidence. That predictability feeds both the FCFF projection and the multiple, because buyers pay for systems, not heroics.

Get Your Agency Valuation in Ten Minutes and Keep It Live

The practical barrier to how to value an agency business has always been time and expertise — running three institutional methods correctly required either a $30,000 appraisal or weeks of spreadsheet work. XIT Matters removes that barrier.

Connect your accounting data via QuickBooks or Xero compatible export, or enter your normalized financials manually, and the engine produces the full three-method stack plus the Blended View in roughly ten minutes. The agency multiple band — 2.5× low, 4.0× median, 6.5× high — is built in, with premium and discount drivers visible as live sliders alongside the output.

Real-Time Slider Modeling lets you drag retainer percentage, owner-dependency level, client concentration, and team bench depth and watch every method and the Blended View recalculate instantly. The AI Scenario Analyst converts plain-English questions — "what if I converted two project clients to retainers and hired an account director at $110K?" — into precise lever movements across revenue, margins, opex, multiple expansion, and the final blended number.

Six Persona Views let you switch between owner reinvestment weighting and pre-sale weighting without rebuilding the model. The Cost of Capital Simulator exposes the WACC drivers that shift FCFF value when you change capital structure or benchmark against PE buyer rates for agency acquisitions.

This is how valuation becomes a management habit rather than a pre-sale event. You see which operational decisions compound into exit value — and which ones look productive but barely move the number that matters.

The 2026 Agency Market Reality Check

Strategic and PE-backed agency acquirers in 2026 are more disciplined than the aggregator boom of 2020–2022. Platform buyers are looking for clean retainer bases, documented leadership teams, and multi-vertical diversification — all the factors that drive premium multiples. They are paying up for those qualities and compressing hard on agencies that rely on the founder to hold the client base together.

If your agency already has retainers above 60 percent, no single client above 20 percent, and a leadership team that has demonstrated independence, current multiples in the 5.0×–6.5× range are achievable with the right buyer. If you are still project-heavy and founder-centric, the next eighteen to twenty-four months of deliberate retainer conversion, delegation, and vertical diversification is almost certainly worth more than accepting today's offer.

The framework in this page — and the live tool that automates it — gives you both the map and the real-time GPS. Stop guessing what your agency is worth and start seeing exactly which moves close the gap between where you are today and the number you have earned.

Grounded in the four-lens framework, FCFF/FCFE/EV/EBITDA math, retainer-mix analysis, and owner-dependency examples from Exit Matters Chapters 4, 7, and 9. All case examples are composites drawn from real owner engagements to protect confidentiality while illustrating the decision framework.